Takeoffs Are Optional; Landings Are Mandatory

The wheels barked as they touched down on the runway for the fifth time on that sunny Georgia afternoon. I was practicing takeoffs and landings in a small Cessna 152 with a local fight instructor. I brought the plane to a stop and taxied off the runway. To my horror, my flight instructor (my aviation lifeline) instantly jumped out. Right before he stranded me alone for the first time in an airplane, he looked back and yelled, “Enjoy your first solo flight, and don’t forget: takeoffs are optional; landings are mandatory!”

With that, he slammed the door shut and walked back to the hangar. As terrified as I was, I knew what I had to do… go fly!

What my instructor said has tremendous implications in aviation and in business. Once we take off, we must land. Once we close a deal, we must exit. Technically what he meant was for me to know the way home before I took off. I need to know my course, the weather, and what to do if something goes wrong. Wings up or wheels up, I was going to land that plane. Once you close a real estate deal, you will exit. The question is whether you make money or not.

Like a pilot before takeoff, we can analyze our deals and decide our course of action, including the exit strategy. Analyzing a deal without considering the exit strategy is like taking off in a plane with no knowledge of the area or flying conditions. You can do it… I just don’t recommend it.

In deal analysis, the first step is to start with the exit strategy. Answer these questions to get started:

- Are you trying to make short-term capital gainsor long-term cash flow?

- Are you looking for large checks quickly, or are you looking for income over a period? (For this conversation, let’s assume that you can’t have both.)

- How long do you plan to hold the asset?

- Buy and hold?

- Buy and refinance?

- Is the asset distressed?

- Stabilized NOI/occupancy?

- Repairs needed?

- What type of debt can you get?

- Traditional?

- Creative financing?

- Short term (bridge loan)?

Cash flow and quick profits are usually exclusive to each other. For example, if you are flipping an asset, you don’t usually have much cash flow, and you don’t care because you are making a large profit on the sale (short-term capital gains). On the other hand, if you get an asset at a good price and its cash flows, you may not exit and realize any capital profit for a while. That’s OK because you are cash flowing. To have both at once is rare. Decide which is most important to you.

Each time you analyze a deal, you will decide if the asset, debt, and exit strategy fit your own financial goals. If you need to create a lump sum of cash in a short period, an asset without any value-add would not be the best deal for you. If you need stable income, fixing and flipping properties each time you want to get paid might be too much work. Here is a closer look at a few exit strategies.

Hold and Operate

Legacy wealth is a popular concept in America today. It is a great idea, but it is not always created in the way most people think.

“If a property is making money, why would I ever sell it?”

I get this question all the time. Holding income-producing real estate long term is one of the most profitable strategies, but it may come with some challenges. Are you using investors’ money, called syndication, to buy real estate? If the answer is yes, then you need to consider who this investment is truly meant to serve. If you think that you will buy real estate for your grandchildren to own and that you will do it with investors’ money, think again.

Investors basically want to know two things when they invest in something: how much money they will make, and when will they get their money back? If you answer, “You will make lots of money in fifty years when my heirs all decide to sell the property,” there may not be many investors who are interested in doing business with you. If you are using all your own money, then holding the building long term may be a more viable option, if you are using investors’ money, then you should always consider a hold time and an exit strategy that will serve them as well as yourself. If you can refinance and give back the investors’ money, that might be different.

Buy, Renovate, Rent, and Refinance

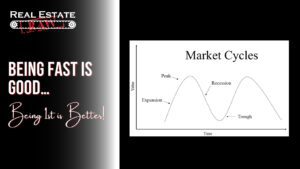

This is the most common strategy in commercial real estate investing. It works extremely well—until it doesn’t. It’s most successful in an upswing economy when values are rapidly on the rise. When the market cycle is in decline, this technique does not work well at all.

The basic concept is that you will buy an asset, fix it up, and stabilize the rents and collections. Once you have renovated the property, you go to a lender and refinance it, pulling out all your cash and having an infinite return on your money. It’s a great idea as long as it works. Here is something to consider when contemplating this exit strategy: When can you refinance the property? When you increase the asset by approximately 30 percent and after the seasoning period (more on this next).

The key concept here is loan to value (LTV). A typical lender with a typical loan will allow you to borrow about 80 percent of the appraised value or purchase price (whichever is lower). When purchasing an asset, usually the appraised value is more than the purchase price, so you put down 20 percent of the purchase price and borrow the other 80 percent. In a refinance, you already own the asset, so there is no purchase price, only the appraised value. This is why I say that you must appreciate the asset by about 30 percent before you can refinance and pull out the 20 percent down payment (and closing costs).

Here’s an example. If the original purchase price is $1 million and the LTV is 80 percent, you will put down $200,000. For you to refinance (assuming 80 percent LTV) and pull out the $200,000 plus closing costs, your assets will now need to be worth about $1.3 million.

$1,300,000 × 0.80 = $1,040,000

$1,040,000 – $800,000 (original debt) = $240,000 (cash-out)

What if I buy an asset at a great price? What if I get an asset for 70 percent of the market value? Can I refinance the next day and pull all my cash out? Technically the answer is yes, but that would be unlikely because of the seasoning period.

The seasoning period is the amount of time that a lender would want you to have owned the property before you can refinance and pull out any cash. This can be from zero days up to 180 days or more and is up to the lender. The best thing to do is to reach out to lenders to get an idea of the standard seasoning period before your initial purchase.

I saved a student from a certain foreclosure not long ago. My student had found a deal that was highly distressed and would not qualify for traditional financing. He was able to get a hard money lender to quote him a loan with a 15 percent interest rate. He knew that the deal could not cover that high monthly payment for long, but it was OK because he planned to close the deal with the hard money lender and then quickly refinance to pay off the loan.

I explained the seasoning period concept and suggested that he call some local lenders to discuss this before he closed with the hard money loan, expecting a quick refinance. The next day he told me that all the lenders would need to see him own the asset for one year before they would even consider letting him refinance. He would have never made it the twelve months with the large monthly payments he would have had to make to the hard money lender. He would have gone into foreclosure long before he was able to refinance.

Don’t forget the seasoning period! You will not only need to force the value of the asset up by 30 percent or more but also need to own the building for an average of twelve to eighteen months before most lenders will allow you to refinance and pull out all your cash. Keep this in mind when analyzing a deal with the buy, renovate, rent, and refinance strategy.

Selling

“You make money when you buy.”

I call bullshit on that age-old real estate adage. It’s not only untrue but also terrible business advice. Ask anyone who has lost an asset in a foreclosure if they made money when they bought it. You create value when you buy, but you don’t make money until you exit the deal, and the check clears the bank. Thinking you have made money simply by buying something completely mitigates the value of an exit strategy. If the exit strategy doesn’t matter, then we can buy anything anytime and we should make money, right? Wrong!

Real estate is based on the greater fool theory of investing. If you buy something at a price, you are hoping that there is someone else (a greater fool) who is willing to pay more for it than you did. Why would they do that? Because presumably the asset has become more valuable during your ownership. Following the greater fool theory makes real estate prices highly market sensitive. Here are some strategies for selling.

Prove the Model

When renovating a property, you may find that you need only to renovate some of the assets to prove the business model but that you may not need to finish the project to get a great price. This is most evident in multifamily properties. I have renovated many properties, but I have never completely renovated any one asset.

To get the best price when selling, a buyer will typically want to see two things—that the asset still has more value-add and that the business model has been proven. For example, if you bought a one-hundred-unit apartment complex with the intent to renovate units and grow the rents, you may need to renovate only ten to twenty of the one hundred units.

Start by renovating 10 to 20 percent of the apartments and lease these units for a rent premium. By renovating only 10 to 20 percent of the property, you will have proven the business model but also left the other 80 percent for the next buyer. You will likely be able to sell this asset for a higher price by showing the buyer a proven path to revenue. The buyer will be purchasing your asset on a pro forma basis, but the model will have been proven. If you complete none of the renovations, then a buyer will likely discount your assets because of the inherent risk of being the first to try to prove the model in that market.

Selling Multiple Assets

Having multiple assets under one loan (umbrella mortgage) can limit exit strategies. When purchasing multiple assets, it may seem like a good idea to bundle them all into one loan, especially if you are buying them all from one seller, but this can have a hang up to it. Most lenders will not allow you to pay off an asset at a 1:1 ratio when there are multiple assets collateralizing a loan.

A good rule of thumb to follow when planning to sell off individual properties from under one loan is to expect a 125 percent payoff. For example, let’s assume that you have ten houses in a portfolio and all under one loan. The loan amount is $1 million. If we divide the total loan amount by each house, then there is only $100,000 worth of debt on each house.

If you sell one house from the package of ten, the lender is highly likely to make the payoff amount for the one house to be $125,000. If you continue to sell the houses at this rate, you will own the last 2.5 houses free and clear before they are all sold. Not all lenders operate the same, so you should check with a lender on this concept before you purchase multiple assets under one mortgage.

If you are dealing with single-family houses or small commercial assets, this will be less of an issue. When you are considering larger assets, you will want to get individual loans on each property. The amount of money you might save in closing costs is negligible compared with the value of being able to sell/exit each asset separately.

Big Town versus Small Town

I have found that in a larger city, you can sell almost any size asset, but in smaller towns, larger properties can be harder to sell. In smaller towns, most buyers are local residents, not institutional buyers. In big cities, you have local and institutional buyers.

Institutional buyers pay well but usually buy only large assets, whereas local buyers tend to buy only smaller assets local to them. Keep this in mind when considering the exit strategy of selling in a smaller city. What size assets are you buying, and what will the buyer pool look like when you are ready to sell?

For more information like this check out my blog at www.realestateraw.com and join my Facebook group Real Estate Raw for Multifamily Investors.

Best of luck!

Bill Ham