Anyone who says that the pen is mightier than the sword never brought a pen to a sword fight.

In the multifamily real estate business money is made on the spreadsheet. Well, it’s lost there too. Overestimating future revenue while underestimating future expenses is one of the fastest ways to fail in real estate. This is what I call pencil whipping a deal. Never pencil whip a deal. You can make any deal look good on paper, but can you bring those projections into reality?

A pro forma is simply a business plan. In real estate, it is a financial projection of the income and expenses (and renovation costs) for a property. This is usually projected in twelve-month increments. Creating an overly enthusiastic pro forma that can’t actually be achieved in the operations of the asset is as smart as bringing a pen to a sword fight.

Your pro forma will start with the initial financial analysis. First determine the financial viability of the deal (CoC, IRR, DSCR) based on the seller’s NOI (from the T12) and purchase price.

Note- if that sentence didn’t make any sense go to the bottom of the article for definitions and to my site www.realestateraw.com to read other articles with full explanations and uses on these terms.

Once you have completed that, the question becomes, does the deal produce a return on investment (ROI) that is satisfactory? If the answer is no, then you must decide what it would take to fix the deal.

The pro forma is your mathematical answer to this last question. It is a financial projection of where the property must be to achieve your cash flow needs. The first thing you must understand is that you will analyze many deals that don’t have any reasonable path to cash flow. Overpricing is the usual suspect, but major capex needs can also be a factor. The pro forma is separated into two sections: physical and financial. Once analyzed separately, the two will be considered collectively.

This is where the cost basis comes in. Simply put cost basis is the total amount of money you have tied up in a deal. This is the purchase amount plus renovation costs and closing costs. This total amount is the cost basis. The cost basis will need to be at least 20 percent less than current market comparable sales for similar assets. Why bother fixing up an asset if it will only be worth the invested amount you have in it?

When you tour a property for the first time, look for the obviously needed repairs. Look at the condition and age in general. You will have time to have the buildings professionally inspected during the due diligence period (once under contract). Ask the realtor what they have underwritten for repairs and upgrades to also get a feel for what is needed. Now that you have your cost basis, you can create the financial pro forma.

Starting with the cost basis, decide what type of loan would be the best fit for this asset. Is the asset in distress or performing? If the asset is performing, you will be able to get the best financing. If the asset is distressed because of low occupancy or lack of repairs, the lender is likely to lower loan to value (LTV) and raise interest rates. This is what we call bridge financing. The loan will be shorter in loan term with a higher interest rate, but that is to be expected when dealing with a riskier asset. Remember, lenders are sensitive to the asset’s debt coverage ratio (DSCR).

Now is a good time to reach out to lenders to see what type of financing would be available for this asset in its current condition. For your analysis, start with the total cost basis and subtract the amount of cash coming from the lender’s proceeds. The difference will be what you need to bring to the project in cash (down payment + closing costs + renovation costs).

Now that you have calculated the amount of capital you will need to bring to closing, does the deal cash flow enough? If not, then you will need to lower the price or increase the NOI to get the cash flow to reach an acceptable level. Let’s assume that you cannot lower the price. Your only option is to increase the NOI. There are only two ways to increase the NOI of an asset: increase revenue or decrease expenses. Let’s look at each separately.

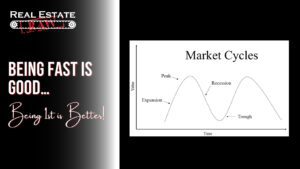

This is easier said than done and is sensitive to the current economic market cycles. When times are good, rent goes up. When the market cycles down, rents can stagnate and even decline in some asset classes and in some markets.

The basics to increasing revenue through increasing rents is a simple supply and demand model. If you have population growth in your area and there are a finite number of apartments to be had, rents go up. If you have population decline in your market, you will see rents soften. If you have job growth in your area, you will typically see population growth. If the market does not provide economic opportunities for people, they will leave. Before you project rent growth in your area, take a long look at the population trend data.

Tip: Don’t use raising rents in the future to justify overpaying for an asset today.

When trying to decide if current rents are below market, you will need to rely heavily on comparable data from other assets in the area. Be cautious about using the comp data provided by the realtor. This is reference information only.

I suggest doing what is called a market survey in the property management business. This is a fancy way of saying to call the competition and see what they are renting their units for. You can also go online to see what similar units are renting for. Do your homework.

Besides comparing unit to unit when looking at rents in the area, be sure to track the rent per square foot also. Take the rentable square footage of a unit and divide it by the rent to get rent per square foot. This data can also be found in offering information from other realtors on other listings. A two-bedroom apartment at your property may rent for $1,000 a month, and a two-bedroom apartment down the street may rent for $1,200 a month. You might think your rent is $200 below market. Maybe they are, or maybe the other units are larger. This is why you compare rent per square foot, not just total rents per unit.

There are two types of rent growth: organic and forced.

Organic rent growth is the amount of rent you can increase at the renewal of a lease without doing any major upgrades to a unit. In most markets, in most economic cycles, this is usually around a 2 to 3 percent annual rent increase. Unless your market is doing extremely well economically and supply and demand is in your favor, you will likely have to upgrade a unit to get a substantial rent increase above organic growth. This is forced rent growth.

I have covered renovating units in other info available on my site www.realestateraw.com, but for now, assume that if you are raising rents, you are renovating units. Is it worth it? When trying to decide if a property should be renovated to capture forced rent growth, you should consider what you can get for nothing—organic rent growth.

Recently I met a realtor for a property tour. The manager was so proud that they had completed the unit renovation on the property. The place looked great. The units were recently remodeled with all the latest touches—new paint, carpet, and light fixtures; modern appliances; and on-site amenities.

I asked the manager, “How much of a rent premium are you getting for these newly renovated units?” She smiled and proudly stated that they were getting a $100 rent bump for spending approximately $4,000 per unit in upgrades. I said, “That’s great! How much are you getting in rent growth when renewing a lease for an unrenovated unit?”

She sheepishly looked at her feet and said, “Seventy-five dollars.”

This manager was spending $4,000 per unit in upgrades to get a $100 rent increase when she could get a $75 increase for doing nothing. She was spending $4,000 per unit to get a $25 rent increase. That’s not worth the trouble. Buying an asset in the right location with the right metrics to the market will allow you to be more profitable with less risk. Location, location, location.

Now that you know how a pro forma works, let me show you how to create one quickly or with limited data from a seller. This five-minute pro forma is used to quickly estimate a rough value for an asset. This will give you an idea of how over- (or under-) valued the sales price is.

The first step is to estimate the revenue for the property. Then subtract the estimated expenses to create the projected NOI. The revenue can quickly be derived using the rent roll. Take the total possible rent for one month and multiply by twelve. Now subtract vacancy (I use 10 percent when estimating). Once you have the total projected rent for the year, you can estimate the expenses using a percentage of the total income. There is no exact science to expense ratios in multifamily homes, but here are some things to keep in mind:

- Ten to thirty units: Operating expenses are about 20 to 30 percent of rental revenue.

- Thirty to fifty units: Operating expenses are about 30 to 40 percent of rental revenue.

- Fifty to seventy-five units: Operating expenses are about 40 to 50 percent of rental revenue.

- Seventy-five to one-hundred-plus units: Operating expenses are about 50 percent of rental revenue.

Note: Operating expenses are all costs associated with daily operations of the asset but do not include debt service.

Once you have determined the gross scheduled rent for the property, subtract the appropriate amount of expenses for the asset size. This will give you an estimated NOI. If you do not have a rent roll, the same data can be recreated by researching other units in the area around the subject property. Do a market survey to decide what the market rent is. Use this to calculate the estimated revenue and NOI. With the estimated NOI, you can calculate the value or the cap rate.

Occam’s razor can be simply stated as follows: When given two explanations for something, the easiest answer is usually the correct one. This is a great philosophy to cut through most of the false information in the world. I have created a system for analyzing the rent growth potentiality of a subject property in any market. I call this the rent razor. When applied correctly, it will cut away all the realtors’ sales pitches on how you can raise rents on an asset. If you can actually raise rents, then the razor will prove that too.

In the United States, a residential rental unit is considered affordable if it does not consume more than 30 percent of the renter’s total income. When a renter’s cost of living exceeds 30 percent of their income, they are rent burdened. This is an especially important concept to keep in mind when considering raising rents for an asset. Will the general population in a market be able to afford the new rents?

To make use of this concept when analyzing a deal, you must know the median per capita income in the area surrounding your property. This data is easy to find with a quick online search. Also, you can go to the Department of Numbers (www.deptofnumbers.com) or the US Census Bureau (www.census.gov) for most of the information.

Note: I use per capita income for this calculation and not total household income. In my experience in property management, 80 percent or more of the rental applications are from single individuals. There may be more residents living in the apartment, but more than 80 percent of the time, there is only one income reported for the application.

Once you have determined the per capita income for the area, now consider the income criteria for leasing a unit of the subject property. How much income must you have to qualify to live at this property? If you don’t know, then use three times the income to rent as a rule of thumb. For most apartments, a prospective renter will need to show that they have a gross monthly income of at least three times the monthly rent.

Per the median per capita income in this market, what percentage of the local population can afford to live at your property? What is that number after you raise the rent? A newly remodeled property is nice but pointless if no one can afford to live there. As your potential renter base falls below 50 percent of the general population, your operations and occupancy will start to struggle because of the lack of the unit’s affordability.

If a unit is overpriced, it is likely to sit on the market longer. Your management company is typically incentivized by occupancy and collections. If you raise rents to the point where your potential tenant base shrinks too much, the management is very likely to lower the leasing criteria to increase that customer base while keeping the rent rates high. This is a mistake.

This will allow the management company to collect move-in fees and to guarantee the occupancy and gross income (that they use to pay themselves). The lowering of leasing criteria will result in higher tenant turnover. The management will get paid but at the sacrifice of the NOI and subsequently the cash flow. Making a unit ready for occupancy after a move out is the largest expense in residential real estate. You can literally raise the rents into unprofitability. How do you think I know this?

When a real estate agent tells you the rents are low, trust but verify. The rent razor is the solution. This method for calculating the affordability of future rent rates will keep you from pencil whipping a deal. Don’t turn a blind eye to data you don’t like. If the math says that the rents cannot be raised, you are significantly raising the risk factor of the deal by assuming that they can. Don’t argue with math.

Valuation through Operation, Not Renovation

When the economy is in a declining cycle, value-add moves into the expense side of the business and away from the income side. Rent growth typically stagnates or even declines in economic recessions. Finding ways to improve a property’s NOI is not as easy as just upgrading the unit and raising rents. Inexperienced investors tend to turn a blind eye to this concept when reaching the peak of a market cycle. It’s easy to convince yourself that a great market could never go bad when you and everyone else around you seem to be printing money in real estate. But it always does and always will. Market cycles are a simple force of an economic nature that don’t need our belief in them to exist. They just do.

Whether at the top of a market cycle or in a declining cycle, your best value-add strategy will be to identify assets that are underperforming for some reason—assets that can be easily fixed without renovating the building itself, just its operations.

With this strategy, you will be able to increase your NOI by cutting costs and operating a more efficient business model than the seller. Identifying weaknesses in an asset starts with the T12. Look for high expenses.

The fastest way to analyze a deal with this approach is to look at the operating expense and the operating expense ratio. Operating expense is the cost of operating the asset for a one-year period. In a multifamily property, it would then be divided by the number of units (doors) to get a per door number. The operating expense ratio is the percentage of operating expenses to income.

Operating expense ratio = Total expenses / Total revenue

Knowing a property’s operating costs and expense ratio is valuable only as a comparison against other properties in the area. Does the subject property have higher expenses than similar assets in the market? Do you know what the average expenses are for other assets in the market?

This is comparable expense data. You will need to track this information the same way that you would track sales prices for similar assets in the area. When you analyze deals, make a point to note the expenses per unit (multifamily) and the operating expense ratios for deals in your market. Get this number by dividing the total annual expenses on the T12 by the number of units. This will give you an operating expense in dollars per door for this deal. Compare this with other assets in the area. Compare the deal’s operating expense ratio with similar deals as well. Track this data regularly to understand assets in your market.

I found one of my most profitable deals by noticing an outlier in the expense ratios when analyzing the deal. It was a large apartment complex (over two hundred units) that included two smaller properties that were about one mile apart from each other. I was buying both assets as one purchase. When analyzing the deal, I noticed that the overall expense ratio was out of line for what I would consider normal operations. The per-door operational costs (operating expenses) were higher than any other asset I had looked at in the area.

When I noticed this, I delved deeper into the financial data. I went through the T12 line by line, looking to isolate exactly where the expenses were high. I wanted to see if this would be something I could fix. Upon closer inspection, I noticed that the payroll was out of whack. My rule of thumb for employees is about two per one hundred units, and the payroll data showed salaries for about four people per one hundred units, which was too high. This expense was equal to about ten employees on a property that should have had only five.

I realized then that I could cut staffing to an appropriate level and add that income back to the NOI. I did this and recalculated the deal. Its cash flowed just fine. I had found a deal! Restructuring the staffing would be something I could do on day one. The next step was to tour the property.

During the tour with the realtor, I asked the property manager how many people worked on the two properties. She explained that the staff floated between the two properties, managing them both as if they were one large property. This was easy to do as they were so close in distance to each other. I asked again how many people total. She said, “Oh, we only have five staff between the two.”

The P&L for this portfolio showed annual salaries equaling about ten employees, but on inspection, I found that there were only five. Where was that extra money going? I will let you draw your own conclusion on that one, but I realized that this was a great deal in hiding. I took over the property and kept the five employees, and it cash flowed nicely. Even better, I didn’t have to fire the five extra staff members because they never existed.

Once you identify that the asset is operating with higher expenses than it should, you need to ask two questions: what and why? Go through the T12 line by line, looking for the exact expense that is higher than average for similar properties. Now that you know what is wrong, you need to determine why it’s wrong.

What has occurred over the past twelve months that has caused this high expense, and can it be easily fixed? The idea is to find property with operational value-add that can be corrected quickly and with little expense. Renovating units and raising rents can take months to accomplish. Operational value-add can often be achieved immediately or shortly after purchasing the property. Here are a few areas to consider.

Management companies tend to overstaff properties. They are typically paid and incentivized on rent collections, not on overall expenses or cash flow. Some management companies charge per hour for their employees’ service.

In this case, the management company is more profitable by overstaffing your property. My rule of thumb is two employees per one hundred units, one maintenance staff and one office staff. Inflated payroll is a great place to look for value-add. By lowering the payroll costs, you can increase your NOI the day you take over the property.

Capital Expenditures above the Line

Some owners will record capex as operating expenses. This is incorrect accounting. Capex should be below the NOI as far as a P&L statement is concerned. By taking the capex as an operating expense, the seller is lowering their NOI and paying less taxes on cash flow. The low NOI will give you a false analysis and an artificially low cap rate.

When you find that a seller is recording capex above the line, add that capex expense back to the NOI and reanalyze. You may find that if you don’t cheat the IRS by recording capital expenses as operating expenses, the deal works just fine.

If you see that a seller is replacing HVAC units, appliances, and hot water heaters on a regular basis, check to see if they have a warranty tracking system in place. Most capex items like this have a warranty on the items that last for months or years. This is applicable only if the management cares enough to file the warranty card and to remember to check it if the part breaks.

I found a property once that had extremely high appliance costs. When I inquired about their warranty tracking system, they had no idea what I was talking about. It quickly became obvious that every time an appliance had any type of problem, the maintenance staff would claim that it was “broken.” They would throw it out and tell the manager that they needed to buy a new one. Pure laziness was costing that owner a small fortune in appliance expenses for items that were still under the manufacturer’s warranty.

Look for a sudden spike in water charges on a T12. You can spot a plumbing leak on a P&L if it is in a month-to-month format (T12). You will see a rise in water costs. Sometimes this is a sudden jump in the numbers from one month to the next, and sometimes it’s a slow rise in costs. If you see a sudden jump, you probably have a single large leak that can be fixed shortly after closing for an NOI bump.

If you see a slow rise in water costs, be more cautious. This could be an indication of a plumbing tsunami coming at you. The slow rise in the water expense may be indicative of slowly failing plumbing—leak after leak that adds up over time. This is probably just deferred maintenance, and you will want to discount the price of that asset to cover the replacement costs for new plumbing.

Tip: To look for high water usage, you can’t always look at the cost in dollars but in gallons used per day. Utility costs vary greatly from county to county and do not provide consistent data to track. To truly know if a property has high water costs, you must measure the usage in gallons per day.

In my experience, the average apartment will use ninety gallons of water per bedroom per day. Get usage data from the utility company that serves the property to find out how many gallons of water it uses a month. Once you have the total gallons used in a month (on the water bill), divide that by thirty for an average daily use. Then divide that number by the total number of bedrooms on the property to determine the daily usage.

Turn costs, or makeready costs, are the expenses associated with a tenant moving out and the management making the unit ready for the next tenant. This usually consists of painting and cleaning the apartment and possibly replacing the appliances. Don’t confuse a general makeready with fully renovating an apartment.

When looking at a T12, it’s not the total amount of money spent turning each apartment; it’s the frequency of those turns that is the real data to track. Are tenants moving in and out regularly? This is bad if they are. Tenant turnover is by far the highest expense in residential real estate. On average, the longer a tenant stays in the apartment, the more money you will make.

Tenants tend to stay in apartments for an average of two years. This translates to a 50 percent turnover in occupied apartments each year. If you can keep your turnover less than 50 percent, you are doing good. If you see that a property has a higher turn rate, ask why.

The answer may be that the management is not screening tenants properly and is leasing to unqualified applicants. This would be upside potential. Do a better job leasing the units to begin with and the tenants will move out at a lower rate.

The other answer may be that the management is doing the best they can with what they have to work with. If the buildings themselves are old or in disrepair, this will greatly affect the quality of the tenant base. Also, if the property is in a high crime area, the tenant base may be less stable. This is not an easy operational fix, and this type of asset should be avoided by the less experienced in this business.

I have found all kinds of expenses on P&L statements over the years. I have seen owners renting apartments to family and “friends” for $1. I have seen an owner who regularly put his private jet as an operating expense on the P&L. You never know what you will find.

Look for unnecessary expenses that can be reasonably cut without affecting the operation of the property. Large corporations that own real estate tend to put corporate expenses on these assets. Travel, employee training, corporate overhead, and partnership expenses are a few of the most common I have encountered. Most of these can be cut to instantly increase the future NOI.

Tip: Watch out for low income creating a false high ratio for expenses. Keep in mind that expense ratio is the ratio between income and expenses. If the income is low, you will get a false high ratio for expenses. If, upon your initial analysis, you find a high expense ratio, stop and make sure that the income for the property is where it should be.

For example, if you have a property that is collecting 100 percent of the rent and it has a 50 percent expense ratio, that ratio will increase if the collections drop (operating expense ratio = expenses/income). Low revenue can give you a false read on the expense ratio and could make you think that there is more upside on cutting costs when, in reality, the expenses are fine. It’s the income that is low. For a double check on this, use the per door expense number and compare that with other assets in the area to see if expenses are high or if revenue is actually low.

I strongly suggest asking yourself this question when analyzing a deal with an operational value-add strategy. This is the “why” question that I posed earlier. Why has the seller allowed this operational failure to occur in the first place? Does the seller hate money? Probably not.

It’s your job to determine what has gone wrong in the operations of the asset and whether it can be fixed. Not all problems can be solved. If there are operational problems, is it that the seller is not aware of the issue, or can it not be solved at all?

This is most evident in the statement that realtors love to use: “The rents are below market!” Yeah, maybe. If the rents are below market, why didn’t the seller raise the rents if that is so easy to do? Does the seller hate money? Are the rents low, or is this a realtor sales pitch?

In many cases, what seems like an easy strategy to cash flow is really someone stepping into someone else’s problems. Before you believe any strategy that a realtor suggests for an asset and before you believe in your own pro forma, make sure that there is a good reason the seller didn’t already enact this plan. I doubt it’s because they hate money. Can it be done? Find out.

Assume that the deal is bad. Assume that the realtor and seller are lying to you. Assume that the problems you have identified are not fixable. Now analyze the deal. Poke as many holes in the analysis as you can. When you can no longer prove that the deal is bad, you have a good deal. In the world of business and real estate, skepticism is not only healthy but also a survival tool.

Tip: I hear people say all the time that they don’t buy on pro forma. This has become such a common phrase in real estate that I feel people have lost the initial meaning. You don’t buy assets based on the realtor’s pro forma, but you do buy based on your pro forma. If you analyze a deal and project cash flow for the next year, that’s a “pro forma”. It’s imperative that you create your own financial projections for a deal and use the realtor’s projections as reference only.

Resident Utility Bill Back System

The resident utility bill back system (RUBS) is a function of the landlord billing the utilities (usually water) back to the tenants. There are companies that specialize in billing back utilities to residents and that monitor those systems for you. A manual way of doing this would be to take the total amount of the utility invoice and divide the total by the number of units, therefore billing it back to the tenants equally per unit. Another way would be to take the total square footage of all the living space on the property and divide the utility bill by that number. This would allow you to invoice residents per size of their apartments. Larger floor plans would pay more of the cost than smaller units.

There is no set way to implement the bill back system, but one thing to keep in mind is that in most states, it is illegal to “sell” utilities to tenants. For this reason, most owners and operators will bill back only 90 to 95 percent of the utility invoice. This ensures that they are not accidentally profitable.

Before you think that you have found free money hiding on a T12 (sellers financials), let me explain a few catches with this system. Billing back utilities to a tenant is the same as raising rents. Do you think the tenant cares what you call it? Bill back, RUBS, utility charges—it’s all a cost-of-living increase to the tenant. It’s the same as raising rents.

If you plan to raise rents and implement a RUBS on a property, you should carefully apply the rent razor to the new total amount that it will cost to live at your property each month (rent + RUBS). How does this affect your potential renter base? This concept is extremely important when looking at properties in towns that have small populations to begin with.

Would you buy what you are selling? This is a final head check when creating a pro forma. Everyone wants to buy a good deal. Does the pro forma you’ve created indicate that this will be a good deal for your buyer or only for you?

Once you have created the pro forma, sell the deal to yourself. Would you buy it? If not, then future buyers (like you) may not be interested in the asset either. If your pro forma shows you are selling at a price that does not create a good deal for the next buyer, then you may be over projecting the future value of your deal.

When considering a future sale price, keep in mind that the cap rate will play heavily into that number, and projecting future cap rates is about as easy as predicting the weather on a certain day five years in the future. Your projected sale price should allow your buyer to create a reasonable CoC return to their own investors and be at a reasonable cap rate.

Remember that your building will age during your hold period. If the market around the asset can maintain its strength, your building will go up in value despite the increase in age. This tends to be true until the building begins to show signs of real aging. Then the building may not appreciate at all. The older the building is when you buy it, the more conservative I suggest you be when creating a future sales price or cap rate. Would you buy it from yourself?

Remember, a pro forma comes in two forms: physical and financial. Renovating properties and raising rents are good ways to increase the value of an asset, but these strategies can be sensitive to market cycles.

Don’t use the idea of raising in the future to justify overpaying for an asset today. Look for ways to increase the NOI by decreasing expenses and operating the property more efficiently to find hidden value in mismanaged assets.

Definitions-

- NOI

- Net Operating Income.

- Total income – Total Expenses (not mortgage) = NOI

- T12

- Trailing Twelve. This is a profit and loss statement in a month-to-month format.

- CoC

- Cash on Cash. This is the return on investment created by the net positive cashflow produced from the project. The formula is-

- Total money invested / Total cash flow.

- IRR

- Internal Rate of Return. This is a complicated formula as you can see below but in layman’s terms it is the total return on investment (ROI) created on a project including cashflow, equity produced at sale, and depreciation.

- DSCR

- Debt Service Coverage Ratio. This is an assets NOI / annual mortgage payment (debt service).

For more information on how to create a proforma or how to use creative financing for multifamily investing go to my site www.realestateraw.com.

Best of luck!

Bill Ham