Step by step instructions to analyze a multifamily property.

The subject of multifamily analysis can be broken down into two key components.

- Property Analysis

- Market Analysis

Multifamily property analysis is the function of arriving at the value of a multifamily property by using three separate valuation methods. These are the income approach, the replacement cost approach, and the comparable sales approach. A market analysis is done by placing the deal you have analyzed into the context of the surrounding market. I will cover the income and replacement cost approaches under the property analysis section and the comparable sales approach under the market analysis section.

Property Analysis

In this section I will show you how to use the cap rate calculation for multifamily properties and how to analyze deals with a cash flow analysis for multifamily investing.

As I stated there are three multifamily property valuation methods. The first step in the multifamily property valuation process is to begin with the income approach. Here is the basic formula for the income approach.

Income Approach

Income – Expenses = Net Operating Income (NOI)

NOI – Debt Service = Cash Flow

Cash Flow / Total Acquisition Cost = Cash-on-Cash Return (CoC)

Debt service is the formal term for annual mortgage payments. Total acquisition cost will be the down payment, closing costs, and renovation costs.

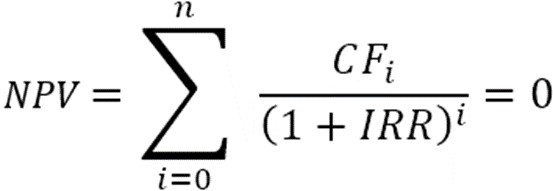

By dividing the total net cash flow by the total amount of cash you have invested in the deal is the return on investment (ROI) produced by the cash flow. Keep in mind that this does not include profit from the sale and depreciation. When these are included in the annual ROI you have an internal rate of return (IRR). Here is the equation for calculating multifamily IRR.

- N = The number of years you own the property

- CFn = Your current cash flow from the property

- n = The current year/stage you’re in while calculating the formula

- NPV = Net Present Value

- IRR = Internal rate of return

Don’t want to do that kind of math? Don’t blame you. To calculate true IRR, you will most likely use a calculator. For a simpler equation, you can use Annualized Return.

Here is the calculation for Annualized Return in multifamily.

(Total Net Cashflow + Profit at Sale) / Total Acquisition Cost = Total ROI

Total ROI / Hold Time = Annualized Return

In this formula the total net cashflow is calculated by adding the net cash flow for each year to get a total dollar amount of cash flow produced by the property for the entire time of ownership.

The profit from sale is calculated by taking the appreciation (difference in your purchase price and your sale price) and adding any equity paydown. Equity paydown is calculated by adding up all the equity that was created by your annual mortgage payment.

Note- equity paydown will only exist if your mortgage consists of a principle and interest payment. If you have an interest only (IO) loan, there will be no paydown of the original loan amount. No equity paydown.

Annualized return is simply taking the total profits created by the sale and cash flow, dividing that by the total cash you have in the deal and then dividing that by the years you owned it.

If you are analyzing a deal for a potential purchase, then you will want to create a proforma for the asset and project the IRR or the average annual rate of return. Be careful when creating a proforma or any future projections. The data you use to calculate the returns (like future sale price and rent growth) can greatly affect your projected IRR or CoC.

Your reputation in the market will depend on your ability to identify quality assets.

Cap Rate Calculation for Multifamily

Understanding capitalization rate (Cap Rate) for multifamily is the second step to valuing a property. Capitalization rate is a “multifunction tool” for real estate and gives many different values for a single asset depending on what information is used for the calculation.

The formula for cap rate in multifamily is as follows-

Net Operating Income (NOI) / Value = Capitalization Rate

In this equation “value” can be one of several different variables. It can be the price you are paying for a property. If can be the price you are selling a property for. It can be a value you plan to arrive at after renovating a property. Cap rate depends on who is doing the calculation and what “value” they are using. It can also depend on whether you are using the seller’s NOI currently being produced by the property or it could be the NOI you are projecting to produce in the future. This would be a proforma.

Simply put, the cap rate is the number of years it takes for the NOI to equal the purchase price. If you don’t have a loan on a property, then the cap rate is also the number of years it takes for the NOI to pay back the purchase price. If you purchase a property with all cash the cap rate is approximately the cash-on-cash return.

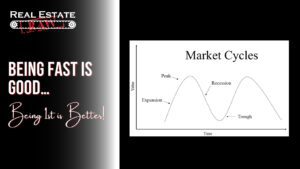

The multifamily capitalization rate can also be considered an inverse relationship. As the cap rate rises or “decompresses” the property is less valuable. As the cap rate lowers or “compresses” the property is considered more valuable. Cap rate compression in the multifamily market is a signal that prices are rising, and prices are dropping if the market cap rate is decompressing.

Another way of looking at a multifamily cap rate is to consider it a metric of comparable sales information. The cap rate shows you how other buyers in a market value a steam of revenue produced by a multifamily asset. For example, let’s assume there is a property for sale, and I offer a price that gives the seller a 6% cap rate based on their current NOI and sale price. You come along with an offer of a 5% cap rate based on the same information. You are willing to pay more for the same stream of revenue produced by this property than I am. All things held equal you will produce less cash on cash than I would because of your higher purchase price.

Here is an example of a property with an annual NOI of $100,000 valued from 4%-7% cap rates.

- Property Value at 4% Cap Rate = Net Operating Income / 0.04 = $2,500,000

- Property Value at 5% Cap Rate = Net Operating Income / 0.05 = $2,000,000

- Property Value at 6% Cap Rate = Net Operating Income / 0.06 = $1,666,667

- Property Value at 7% Cap Rate = Net Operating Income / 0.07 = $1,428,571

- Property Value at 4% Cap Rate: $2,500,000

- Property Value at 5% Cap Rate: $2,000,000

- Property Value at 6% Cap Rate: $1,666,667

- Property Value at 7% Cap Rate: $1,428,571

If you are buying a property for more than the market cap rate you are getting a property for less than everyone else and if you are paying a lower cap rate than the market cap, you are paying more than everyone else.

Operational Cap Rate Decompression.

Value-add for multifamily is the process of increasing a properties value by increasing its net operating income (NOI). Refer to the cap rate equations above. If the NOI increases (cap rate stays the same) the value increases. If you increase the operating performance of a property, you can force appreciation too.

Note- this conversation on cap rate decompression through increased operations does not take into consideration the market cycle in general. If you renovate a property in a market with falling prices, you may not get much increase in the after-repair value (ARV). I made this mistake renovating apartment complexes in the post 2008 market.

Most investors only know of one way to create value on a multifamily property. Fix up the units and charge more rent. This is a good strategy but not the only way to increase the NOI of a property and renovating assets is very sensitive to the market cycles.

Valuation from operation, not renovation, is the key to a long-term value add strategy in multifamily. As the old saying goes- “If all you have is a hammer, everything looks like a nail.”

You need multiple “tools in the toolbox”. Renovation is just one. Look for properties that are distressed in the operations. Cutting expenses has the same effect on the NOI as raising rents. Looks for ways to improve operations as well as renovations.

Again, lets imagine you have a property producing a $100,000 NOI. If we have a market cap rate of 5% this property has a market value of $2,000,000.

What if we can improve the operations and increase the NOI by $25,000?

The value goes from $2,000,000 to $2,500,000!

$125,000 / 0.05 = $2,500,000

As you can see at $25,000 operational improvement adds $500,000 in value. This operational improvement can be raising rents as well as cutting excess expenses. Combine both for a truly successful value-add strategy for multifamily investing.

Cap Rate Caution

Cap rate alone is not enough information to base a valuation on. Look at all three methods when valuing a deal. Cap rate can also be manipulated to create a high projected sale price. This is something to watch when someone invites you to invest in a real estate deal. A low projected cap rate at sale can create large IRR returns. Make sure any cap rates used for the prediction of future value are reasonable. Consider the condition of neighborhood and the condition/age of the building when calculating a value for a multifamily property.

Older properties typically have higher cap rates and newer properties have lower cap rates.

Equity Multiple for Multifamily

Equity multiple is a key metric for a multifamily analysis and shows the percentage of growth of any money invested in the deal. Here’s how the equity multiple is calculated:

Equity Multiple = Total Distributions / Total Equity Invested

Note- total distributions include all the cash flows generated form the property, such as rental income, proceeds for the sale, and other sources of income, minus any operating expenses, debt service, and other costs. Total equity invested is the sum of all the capital invested by the investor/s, including the initial investment amount and any renovation money or contributions made during the holding period.

For example, a 2X multiple would mean that you doubled your money in that particular investment. This would be a 100% return on the investment.

Example- You invest $100,000. The deal sells and you get back $200,000.

This is a profit of $100,000.

$200,000 – $100,000 (initial investment) = $100,000 net profit or a 2X multiple.

If the multiple is 1X then that means you broke even on the investment and anything less than 1 means you lost money. This does not consider the hold time.

Take the total percent return and divide by the years owned to get the annualized return.

Example- If you get a 2X multiple (doubled your money) and it took 5 years to do that, you will have an annualized return of 20%.

100/5 = 20

100% return / 5 years = 20% a year.

Calculating the equity multiple for a multifamily investment helps you evaluate the potential return on the investment by considering both the initial capital invested and the total profits earned over the holding period. The equity multiple provides a clearer picture of the overall performance of an investment compared to just looking at individual metrics like the internal rate of return (IRR) or the cash-on-cash return.

What is a good equity multiple for multifamily?

The answer is obviously an opinion and differs for each investor but typically a 2X or greater return is considered good for a multifamily investment.

Tell me the difference between equity multiple and IRR?

The difference between equity multiple and IRR is depreciation. When you add the factor of depreciation into the annualized return equation you get IRR. The annualized return is the multiplied equity divided by the years held.

Multifamily math is great, but this is still not enough information to make a full decision as to whether the property you are looking at is a good deal or not. Here are a few more decisions to consider when analyzing multifamily real estate.

Age and Condition

With age usually comes a lesser condition. The older the property the more repairs and maintenance may be needed soon. Your job as the analyzer of this property is to take all points into consideration. Hidden repairs and maintenance are a big factor.

Expenses on a multifamily property can be separated into two categories. They are operating expenses (OpEx) and capital expenditures (CapEx). OpEx is the total amount of money spent during the normal operations of a property not including debt service nor any capital expense items. CapEx refers to the spending required to improve, maintain, or upgrade the physical condition and functionality of a property. These expenditures are typically larger, that go beyond routine maintenance.

CapEx should be considered in two forms. Single-event or recurring. If you upgrade, replace, or renovate an item on the property, that is likely to be a single event. Examples of this would be replacing a roof or replacing all the pluming or electrical systems. Once completed these are not things that will be done again for many years if ever.

Recurring CapEx is something that is still considered a capitalized item but may be replaced on a more regular basis. This would be things like refrigerators, stoves, HVAC systems, kitchen cabinets. While you may not replace the same refrigerator in the same apartment each year, you will replace some refrigerator in some apartment each year. Same with other items that may fall under the heading of CapEx, but the expense occurs on a regular basis.

When using any of the discussed multifamily property valuation methods, if you see that the seller has included single-event CapEx costs in the operating expenses of the property, you will want to add that cost back to the NOI before a full analysis. Recurring CapEx should be considered the same as normal maintenance costs and be included in the NOI to be safe. This is what is called the cash flow analysis for multifamily investing.

Multifamily Market Analysis

In this section I will show you how to do market analysis for multifamily properties as well as how to choose a multifamily market for investing.

The first concept is the comparable sales approach. The comparable sales approach is a multifamily valuation method by looking at the cap rate for a property and comparing that to the market cap rate for similar assets in the same market.

Basically, the comparable sales approach is just about looking at what everyone else is paying and deciding if you are paying mor or less than everyone else.

This is one of the main functions of cap rate. The market cap rate for a particular asset would be calculated by taking the average cap rate of all sales for all similar (size, age, location, condition) property in a single market over the past 12 months. If you are paying a lower cap than everyone else, you are paying too much and vice versa.

How to Choose a Multifamily Market

Multifamily market selection is a key subject when building your multifamily portfolio. There are a few key elements to consider such as population growth, job growth, landlord/tenant laws, price, and many more. I will cover these topics, but I will start with a less considered point of view. Can you show up? That’s it.

In my 20 years of multifamily investment experience, I have realized that typically the best real estate deals come through relationships with the active realtors and sellers in a market. The best way to build relationships with people is to physically meet them. In the multifamily arena this is done with property tours.

A property tour is a quick visit to a property to meet the realtor (possibly seller and management as well) for a tour of the asset. This is not due diligence, so you don’t need to be prepared to conduct a professional inspection. Just a meet and greet at the property.

Showing the listing agent that you are willing and capable of visiting the property starts the relationship in a good manner.

If you are not able to travel to your subject market on average once every six weeks, you may want to consider a market closer to your home. Once every six weeks is just an estimate to convey the point that you need to be able to show up on a regular basis and sometimes quickly.

If you don’t show up, a local will. The person who lives in the market is always the greatest competitor to someone who lives in another area. If you are not local, you will have to show up like a local to be competitive in that market.

Good deals don’t stay on the market long and great deals don’t come to the market at all. They are traded privately through relationships.

The needed relationships are with sellers and realtors in the market. If you have relationships, then you will get calls about potential deals before other buyers do. This is why getting to know people in a market is so important.

Simply going online and looking at deals is good to get going in a market, but you will need to move beyond that level of deal flow, if you want to find better than average deals. Properties that are listed on the internet are extremely accessible by anyone with an internet connection. Everyone sees those deals. They are picked over.

Your job is to build relationships with the agents in the market to be the first notified about FUTURE deals. Not the ones for sale right now. How do you build relationships? Show up.

The second most important aspect of market selection is deal flow. By this I mean your market will ultimately be the total area that produces enough opportunities to build your portfolio. Once you have decided what size deal to begin looking for, you need to analyze those type properties on a regular basis (deal flow). I suggest that your “market” is the total area (collection of cities) that produces at least 3 potential deals a week.

Here is a step-by-step process for choosing a multifamily market.

- Pick a starting point such as your personal residence.

- Imagine your address on a map of your city and now draw a large circle around your address on this map.

- Inside this circle you need to find 3 deals a week.

- The circle will grow until you are comfortably finding 3 deals a week.

- The larger the property size you want to buy the larger the circle.

- The circle may ultimately include multiple cities or even states depending on deal size and availability of properties for sale in each area.

If you are trying to buy duplexes or quadraplexes, you can probably keep the circle to one city. If you are trying to buy 200-unit apartment complexes, you will likely have to cover many cities to be able to find 3 fresh leads a week.

Here are a few other areas to consider when choosing a multifamily market for investing.

- Population growth (for the previous 20 years)

- Thirty percent growth for cities with a population of 250,000 or less.

- Twenty percent growth for cities with a population of 250,000 to 1,000,000.

- Fifteen percent growth for cities with a population of 1,000,000 to 2,000,000.

- Ten percent growth for cities with a population of 2,000,000 or more.

- Median household income growth

- Thirty percent or more growth of the median household income over the last 15 years.

- Crime

- Crime should be declining or at least holding steady in the area.

- Job growth

- Two percent or more annualized job growth in the city if the population is less than 1,000,000.

- One and a half percent or more annualized job growth in the city if the population is more than 1,000,000.

- Median household income

- The median household income should be over $45,000 a year for the area.

- Median rent

- The average rent for the city should be no less than $800 a month.

For current data, visit the Census Bureau and the City-Data websites.

For more information like this check out my blog at www.realestateraw.com and join my Facebook group Real Estate Raw for Multifamily Investors.

Best of luck!

Bill Ham